How the Marine Sector Can Help in the Fight against Climate Change

6 November 2019

At Devon Funds we have a long history of engaging with companies on issues associated with the environment, social best practice and corporate governance (ESG). This approach is employed across all our investment strategies but in early 2020 we will also offer an investment fund which explicitly recognizes Sustainability as a key foundation in the construct of a Trans-Tasman share portfolio. We believe that the benefits of this approach will be evident in both improving the return potential of the Fund but also in further representing the values of our clients. In representation of our position on ESG and because our investment process is one which involves deep fundamental analysis, we have written today on our views around the state of the Aquaculture industry in New Zealand and its implications for several of our listed stocks.

The New Zealand Government recently announced its Aquaculture Strategy, articulating a vision to make New Zealand globally recognized as a world-leader in sustainable and innovative aquaculture management across the value chain. In raw dollars the strategy is targeting a rise in New Zealand’s annual aquaculture sales from the current $650 million to $3 billion by 2035 – current progress suggests the industry is already on track to reach $1 billion in annual sales by 2025. This strategy aims to not only further drive innovation in our aquaculture sector, helping to diversify New Zealand’s primary sector economy but also, in alliance with a focus on improving returns from wild-catch fish harvesting, help to position New Zealand in the fight against climate change.

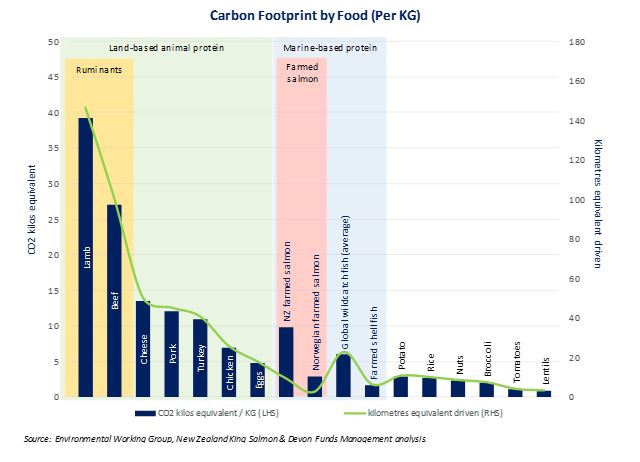

When it comes to climate change, it turns out what we put on our dinner plate matters. Between 25% and 30% of global greenhouse gas (GHG) emissions come from the production of food, which is twice the amount of GHG emissions from the cars we drive. Land-based livestock alone accounts for 14.5% of global man-made GHG emissions (which roughly equates to the GHG emissions from all transportation on our planet) and in New Zealand it has an even larger impact – more than 35% of our GHG emissions come from livestock protein production. One of the key contributors is methane, which is produced in large quantities by ruminant animals and is 25x more potent than carbon dioxide in its green-house warming effects.

The chart below illustrates the carbon footprint from different foods:

In general, marine-based proteins emit much lower amounts of GHGs than land-based proteins. And given the degree to which agricultural methane and nitrous oxide emissions contribute to New Zealand’s total GHG emissions, it is unsurprising that our Interim Climate Change Committee has emphasized that reducing the emission of these two substances is key to our efforts of achieving a net zero target by 2050. Additionally, as a signatory to the Paris Climate Agreement, New Zealand has a nearer-term pledge, which is to reduce its emissions to 30% below 2005 levels by 2030, starting from 2020. Transitioning more of our protein source from land to marine not only helps us lower our carbon footprint, but also supports growth of the fishing and aquaculture sector. We view fighting climate change via innovation in the primary sector as a necessity for a vulnerable island nation like ours. We also believe that as consumers globally become more aware of the carbon footprint of their diet, they will shift their consumption behaviors too, further driving growth in this sector.

Improving marine protein production with as low an environmental impact as possible requires different methods to be used across wild-catch fishing and aquaculture (the farming of fish and shellfish).

In wild-catch, it is not as simple as just increasing production volumes. New Zealand currently has one of the world’s most sustainable wild-catch fisheries, achieved by using a Quota Management System (QMS). While the QMS has some serious flaws, its aim is to keep fish stocks at levels from which they can sustainably regenerate their populations, ensuring that future generations of Kiwis will continue to be the custodians of a biodiverse Exclusive Economic Zone. But the QMS intrinsically limits volume growth, meaning that the only way for our country to grow the wild-catch marine protein sector is to move up the value chain. Companies such as Sanford have already proven that by using smarter technologies such as Precision Seafood Harvesting and on-vessel filleting, they can extract more value out of the fish caught from our oceans. The company recently achieved operating earnings per kilogram of fish of $0.54 in 2018 which was a substantial improvement from the $0.35c per kilogram achieved in 2015. Sanford has the goal of achieving operating earnings per kilogram of $1.00. Part of this value improvement will come from achieving a price premium which reflects the value attached to the sustainable practices of New Zealand’s wild-catch fishing.

Aquaculture, on the other hand, is continuing to see strong volume growth. In 1960 the total global fishery (commercial, recreational and subsistence) was estimated to be around 35 million tonnes, of which 97% was wild-catch. Today the total is over 200 million tonnes and more than half of that is from aquaculture. Moreover, wild catch production has been static at around 95 million tonnes for 30 years – all of the growth since then has come from aquaculture. The reason for this pattern of growth will be unsurprising – we have over-fished the oceans (and at current levels continue to do so) to the extent that increasing production is practically impossible, yet demand continues to grow. If we want to satisfy that demand, then farming fish is the only possible solution.

In New Zealand our aquaculture has also seen significant growth, led by listed companies New Zealand King Salmon (who currently operate salmon farms in the Marlborough Sounds) and Sanford (who operate salmon farms in Stewart Island and mussel farms elsewhere). These companies and others are further investing in our aquaculture sector to achieve both more volume and more value. Companies like Sanford are already turning Greenshell mussels, a species native to New Zealand, into a powder which has promising anti-inflammation properties. They recently announced the results of a breeding programme that showed that selected hatchery mussels could grow up to twice as fast as those caught in the wild. Sanford suggested the economic value of this work to New Zealand could be up to $200m, demonstrating that innovations in aquaculture have both environmental and and economic merits.

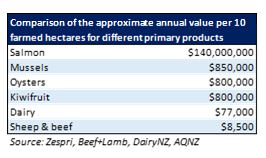

Historically, New Zealand’s aquaculture sector has faced expansion challenges due to the level of competition from other close-to-shore activities. The government’s Aquaculture Strategy aims to increase the efficiency of current farming but also to open up a whole new potential growth area by extending farming into the open ocean. The attractions of open ocean aquaculture are obvious – New Zealand’s exclusive economic zone is 15 times larger than its land mass so space is almost unlimited, and crucially, as the climate warms the need to farm in cooler, deeper water will become increasingly urgent. But the technological challenges of operating in the open ocean are daunting with farms, for example, needing to be able to survive waves of up to 11-meters. However, if these challenges can be overcome, the potential benefits are significant. As the table below shows, the relative space productivity of aquaculture is very high.

The New Zealand marine sector offers great opportunity over coming years as it looks to satisfy a world which is increasingly hungry for quality marine protein whilst having to deal with the challenges associated with climate change. How our listed companies navigate these risks and opportunities will be fascinating. Our approach though is to ensure that we continue to develop our knowledge in this sector and carefully observe the corporate strategies being employed.